How long will the Chinese yuan continue to rise against the US dollar before Beijing intervenes?

- While currency traders have latched onto the yuan’s large interest rate premium as a sure-fire bet, the joyride won’t last forever

- The key issue is how long it will be before Beijing steps in and exercises some restraint

Currency traders have latched onto the yuan’s large interest rate premium as a sure-fire bet, but there is a catch. The joyride won’t last forever and the key issue is how long it will be before Beijing steps in and exercises some restraint.

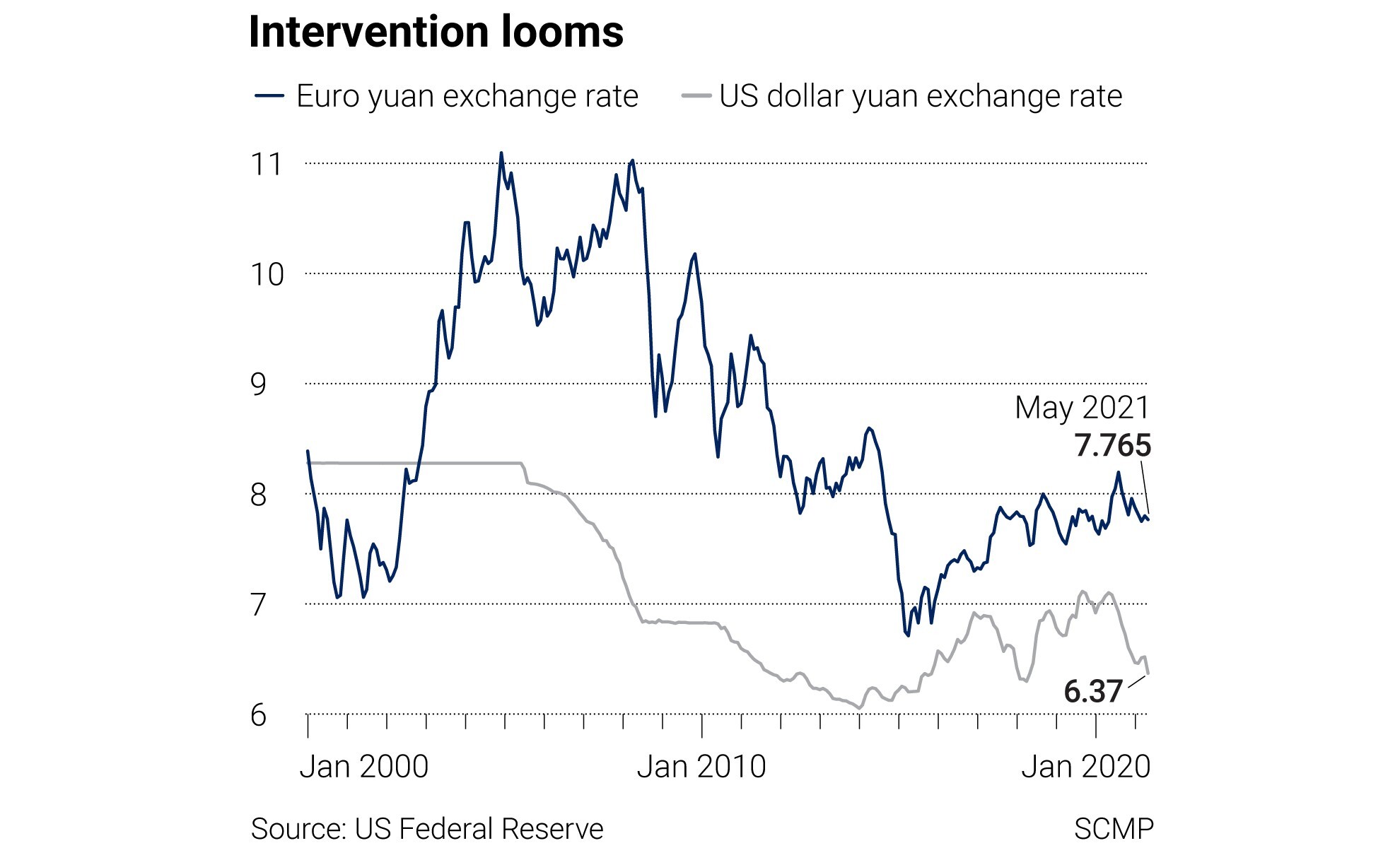

With the currency already running at three-year highs against the US dollar, the risk of intervention by the authorities must be mounting. If the market gets the bit between its teeth, momentum could soon build for a move towards 6 yuan against the US dollar, a level that nearly traded in January 2014 when the exchange rate reached a low of 6.04 yuan.

The trouble is that China’s rock solid economic fundamentals are hard to ignore, with relative growth, interest rate and bond yield differentials all heavily weighted in the renminbi’s favour. They maintain a lot of pulling power.

China’s first-quarter GDP growth rate was 12 percentage points above the US’ and its benchmark interest rates offer a 3.5-percentage-point premium over US rates, while 10-year government bond yield spreads are about 1.5 percentage points in China’s favour over US treasuries.

It’s no surprise investors are so positive about the currency, especially while the global appetite for risk assets remains so upbeat. Over the past year, the renminbi has rallied 11 per cent against the dollar and gained 5.5 per cent versus the euro over the past 10 months. There’s more to come.

With global growth making up for lost time from the pandemic, China’s factories are working flat out as the world rebuilds depleted inventory levels and gears up for faster economic expansion. Even though China’s imports surged by a larger 43.1 per cent in April, it is not making serious inroads into the nation’s trade surplus, which continues to rise exponentially.

02:01

China’s economy expands record 18.3 per cent in the first quarter of 2021

With global demand for China’s manufactured goods mostly ignoring moderate price changes, it will take time before the stronger renminbi begins to take effect and helps cut back China’s trade surplus with the rest of the world. In the meantime, more constructive trade negotiations with the US and Europe will be needed as a stopgap to prevent any further rifts developing.

China still needs to stabilise the renminbi, but policy options are limited. Doing nothing is not practical as the markets will take any hint of currency benign neglect by Beijing as a green light to hit the dollar even harder in the renminbi’s favour. Beijing can ill afford to cut interest rates any further, especially as there are worries that China’s monetary policy settings are already too loose.

In seeing China’s rise as a threat, the US is undermining globalisation

But it can mount a whispering campaign and tacitly intervene, selling the renminbi without making too much of a splash. The markets would soon take the hint. The rise in China’s official reserves to US$3.198 trillion in April suggests that a market-smoothing operation may already have started.

The global interest rate cycle might also begin to turn in Beijing’s favour, especially if market talk continues to build about the possibility that US interest rates could soon be heading higher. The British pound has rallied in recent days on speculation that the Bank of England might tighten policy sooner than anticipated. The clock is ticking for super-low interest rates.

Leaving it to chance is not an option for Beijing. Staying proactive on the exchange rate is the best strategy with intervention looming.

David Brown is the chief executive of New View Economics