People attend a job fair in Chongqing on April 11. China’s reopening, after abandoning its zero-Covid policy, sets it apart from a world economy facing a significant risk of a hard landing this year. Photo: AFP

Opinion

Macroscope

by Nicholas Spiro

Macroscope

by Nicholas Spiro

China’s reopening is weaker than expected but still a rare bright spot amid global economic gloom

The impact of China’s reopening has been muted due mainly to a patchy and tepid revival in economic activity in areas such as property and exports

Even so, it is important to put things into perspective as it is still early days and reopening is taking place amid other market-moving events including the banking turmoil in the US and Europe

Is China’s great reopening living up to expectations? At the beginning of the year, The Economist described the unsealing of China’s borders as “the biggest economic event of 2023”.

At the time, many investment strategists and market commentators took a similar view. They predicted that the sudden end to three years of self-imposed isolation would, after an initial period of turbulence, lead to a sharp recovery that would provide a much-needed counterweight to the monetary-tightening-induced slowdown in the United States and Europe.

Yet, three months on, the impact of China’s reopening – both at home and abroad – has been less dramatic than anticipated. While it is still early days, the post-zero-Covid recovery has been bumpy and underwhelming in many respects.

The abrupt dismantling of draconian restrictions has lost its capacity to move markets. This is partly because it has been superseded by other market-moving events, in particular the banking turmoil in the US and Europe.

Tellingly, searches for “China reopening” on Google Trends, which spiked last December, have almost evaporated in the past several weeks. More surprisingly, Chinese stocks’ performance this year has been relatively lacklustre. The CSI 300 index of Shanghai and Shenzhen-listed shares is up 4.8 per cent, compared with 7 per cent for the benchmark S&P 500 index, despite the fallout from the collapse of three mid-sized US banks.

04:41

Excitement and anxiety as China starts to reopen after zero-Covid

Excitement and anxiety as China starts to reopen after zero-Covid

The renewed escalation in geopolitical tensions – especially across the Taiwan Strait – and persistent concerns among foreign investors about the regulatory regime in China have weighed on sentiment. Moreover, commodity markets have been driven more by fears about a global recession than hopes China’s reopening will boost demand from the world’s largest consumer of raw materials. Even an index of industrial metals, which are more sensitive to Chinese growth, is down 5.3 per cent this year.

Yet, the main reason the impact of China’s reopening has been fairly muted is because the revival in economic activity has been patchy and tepid in certain areas. In a report published on Tuesday, Nomura noted that “while in-person services and mobility have displayed a strong recovery, the property market’s rebound seems to have been short-lived, while exports continue to contract”.

Consumer confidence remains fragile because of scarring from the Covid-19 pandemic and a weak labour market. Household saving deposits have continued to increase, suggesting consumers are reluctant to engage in a spending frenzy. The absence of cash handouts to households to boost consumption has added to doubts over the strength and sustainability of the recovery.

However, it is important to put China’s reopening into perspective. As recently as last October, the odds of a swift and comprehensive dismantling of the zero-Covid policy – which was long viewed by investors as the missing catalyst for a meaningful recovery in Chinese asset prices and economic activity – were slim.

Yet, in the space of a month, Beijing eliminated one of the biggest threats to the world economy. It abandoned its struggle with the coronavirus at a time when global growth was weaker than at any point since the eruption of the pandemic and amid mounting concern about the damage unleashed by an abrupt reopening.

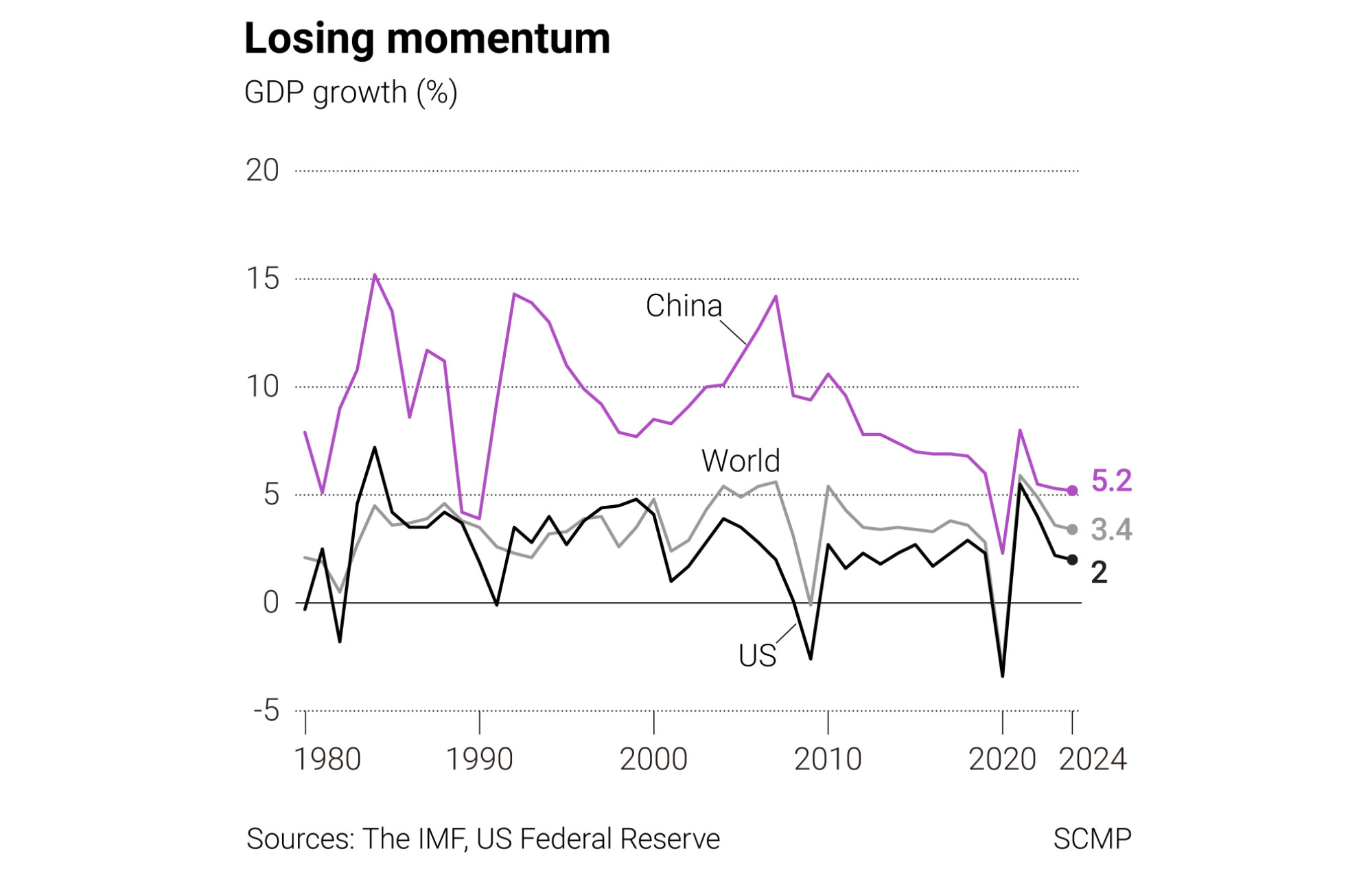

Fears over the government’s failure to prepare properly for a sudden lifting of restrictions convinced some analysts the economy would contract in the first quarter of this year. However, according to JPMorgan, growth is likely to have reached 9 per cent on a quarterly basis and 3.4 per cent year on year.

High-frequency data showed that subway traffic in 29 cities last week was 26.7 per cent higher than the average level in 2019, while international air traffic stood at 41.2 per cent of 2019 levels. That was up from less than 25 per cent in early March, according to JPMorgan data.

Although there are some concerns about the pace of growth – especially once the boost from the lifting of pandemic restrictions fades – the reopening sets China apart from a world economy facing a significant risk of a “hard landing” this year, as the International Monetary Fund warned on Tuesday.

Never mind whether China’s rebound is not as strong and secure as many had hoped. The consequences of a continuation of the zero-Covid policy – which appeared likely only several months ago – do not bear considering.

Furthermore, the global financial and economic landscape has shifted since China reopened. The fallout from the failure of several US banks has caused lending standards to tighten, precipitating a credit squeeze amid persistently high, albeit easing, inflation that makes it difficult for the US Federal Reserve to cut interest rates.

Financial stability risks, although a perennial threat in China, have become more acute in the US. This accentuates the appeal of Chinese government debt for investors seeking to diversify their portfolios. While US bonds have swung wildly since the end of February, Chinese bonds have traded in a narrow range.

China’s reopening has failed to impress markets, but that says more about problems elsewhere in the world. As the outlook for the global economy darkens, China is a rare bright spot.