We may not be headed for global recession gloom after all

- The world is battening down for a long recession in 2023, but the winds may be changing direction

- Energy prices and inflation levels appear to have peaked, interest rates are expected to do the same next year and there is even hope that 2023 will bring more easing of China’s zero-Covid policy

If there is a recession coming, it should be short and shallow and the glut of liquidity left over from collective quantitative easing should ensure that global recovery, when it comes, will still be flush with funds. It’s time to reassess the outlook.

The news has definitely made tough reading through most of the year. The shock of the Ukraine war, the spike in inflation, the drive for tougher monetary conditions by the central banks, and the downturn in global business conditions have, at times, seen investors, consumers and businesses running for cover.

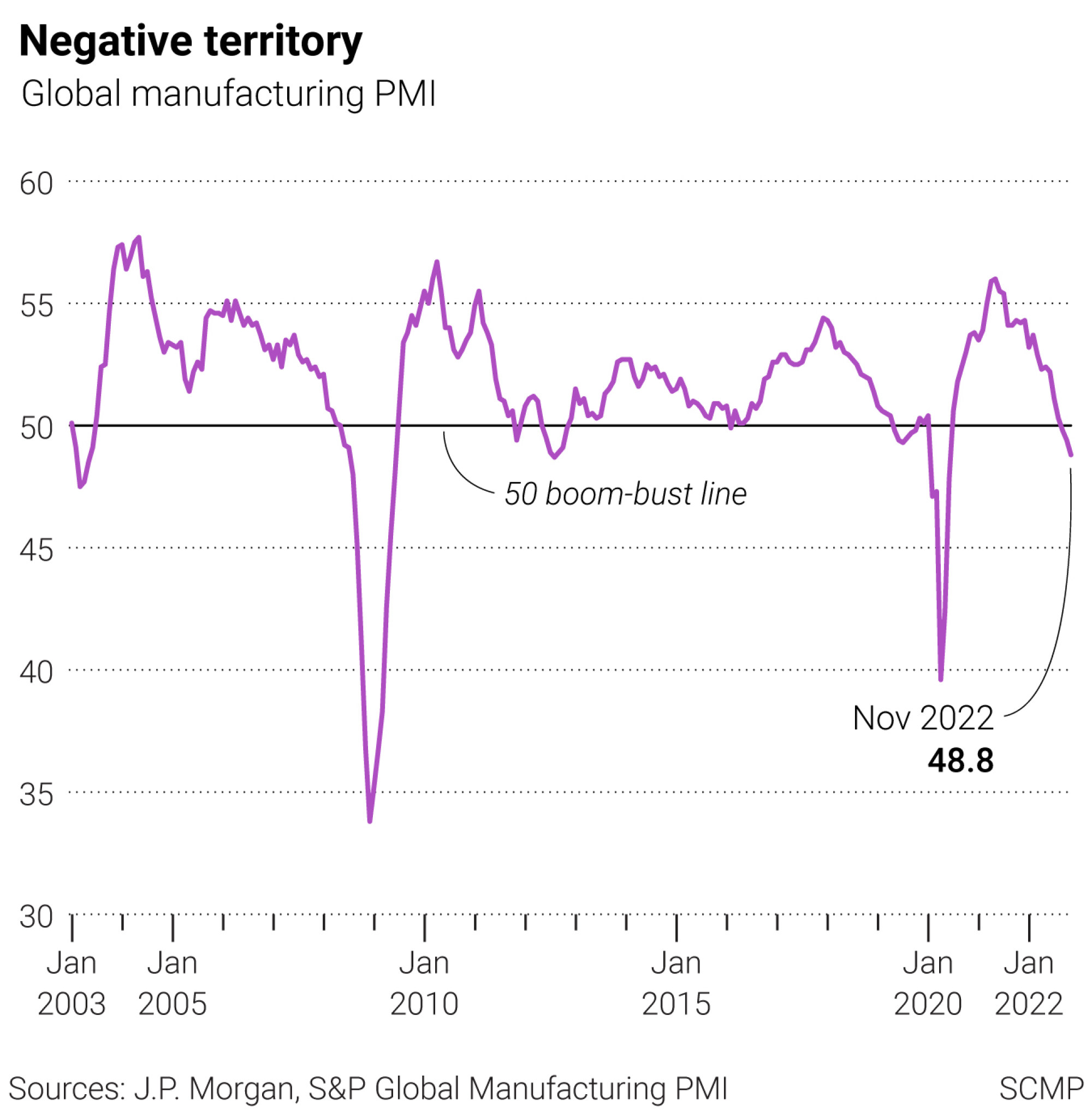

The JP Morgan, S&P global manufacturing purchasing managers’ survey sums up the mood with the PMI index dropping below the vital 50 boom-or-bust threshold for the last three consecutive months, consistent with contracting business activity.

The last time this global manufacturing PMI was in negative territory business confidence was in free fall at the height of the Covid-19 pandemic in 2020. This time though, things should be a lot different.

There are still aspects to draw on for inspiration, not least the possibility that the Fed’s battle against inflation may soon be reaching a conclusion, with clear signs that the headline CPI rate has already topped out. US inflation slowed down to 7.7 per cent in October from a peak of 9.1 per cent in June and the trend should be lower in the coming months thanks to the strong dollar and easier global energy prices.

As inflation risks recede, it should take pressure off the US Federal Reserve to respond with tougher monetary policy ahead. The Fed funds rate, currently in the range of 3.75 to 4 per cent, is expected to peak at around 5 per cent early next year, but the futures market is already factoring in forward interest rates moving back to 4 per cent by the end of 2023 as inflation pressures continue to ease.

, chair of the US Federal Reserve, in Washington, US, on November 30. Powell has signalled that policymakers will soon ease their rapid pace of monetary tightening. Photo: Bloomberg")

The message from US economic indicators is better than expected too, not least the booming US labour market conditions. Last week saw another strong set of non-farm payrolls adding an extra 263,000 jobs to the economy in November, much higher than consensus expectations for a 200,000 gain.

With November’s unemployment rate unchanged at 3.7 per cent, it’s another pointer that the US labour market is operating close to full capacity, good news for consumer confidence down the line.

The Organization for Economic Cooperation and Development (OECD) has marked the US economy down for only 0.5 per cent growth in 2023, but the odds are that its forecast is too cautious and growth should exceed expectations.

2023 will be a better year for investors, even with recession looming

Despite all the talk of an impending crash in 2023, there’s every reason to hope for better times ahead. Global growth could well surprise on the upside in 2023.

David Brown is the chief executive of New View Economics