Live | China Markets Live - Hong Kong shares finish quietly weaker as trade looks to US jobs data

Chinese markets out on holiday, will reopen Monday. US jobs figure may give lead on timing of rate increases by Federal Reserve

Welcome to the SCMP's live markets blog. The intense volatility of recent weeks has every chance of remaining the core underlying theme of activity. Investors are increasingly focused the broader question of how this episode might affect the wider economy as many suspect the equity bubble has yet to fully deflate. We'll bring you the key levels, trading statements, price action and other developments as they happen.

Here’s a summary of market action yesterday and today, with analyst views:

- Hong Kong's Hang Seng index settles slightly lower

- Chinese markets closed Thursday and Friday for holidays, reopens Monday

- Investors look toward US jobs data due out on Friday, US markets shut Monday for Labor Day

- Japan shares finish lower, post 4th straight week of declines

4:07pm: The Hang Seng Index closes at 20,840.61, down 0.45 per cent or 94.34 points. The H-shares index finished at 9,169.59, off 1.42 per cent or 131.73 points.

4:03pm: The shipping and logistics sector traded 1.2 per cent up in Hong Kong’s stock market today, after talk spread amongst market players that China Merchants Group would merge with Sinotrans & CSC.

China Merchant Holdings gained 3. 067 per cent to trade at HK$25.2 with a turnover of 180.79 million, while Sinotrans and Sinotrans Shipping saw an increase of 11.246 per cent and 7.534 per cent in their share prices as of 3:55 pm.

3:12pm: Hong Kong-listed property developers also had a tough day, with the whole sector trading down 1.11 per cent as of 2:44 pm.

Sung Hung Kai Properties lost 0.473 per cent to trade at HK$94.65 with a turnover of 409.05 million. The share price of state-owned Poly Property, among the top 5 mainland Chinese developers, hit a 5-day low, trading down 2.564 per cent at HK$1.9 with a turnover of 36.4 million.

3:10pm: Reuters on Japan's closing market:

Japanese stocks slipped to seven-month lows, with the Nikkei posting its biggest weekly fall in almost a year and a half with speculators dumping futures while investors stayed risk-averse ahead of the release of a key U.S. jobs report later in the day.

The Nikkei lost 2.2 percent to close at 17,792.16, shedding 7 per cent throughout its fourth straight week of declines, its largest weekly fall since April 2014.

The benchmark briefly touched 17,737.01, its lowest level since February 10, with the yen’s gains souring already weak sentiment strained by concerns of a hard landing in China.

3:08pm: The Hang Seng Index trades at 20,860.83, down 0.35 per cent or 74.11 points. The China Enterprises Index (H-share index), which track Hong Kong listed Chinese companies, trades at 9,174.57, down by 1.36 per cent or 126.75 points.

2:44pm: Six major casino operators in Macau saw their share prices rebound today. Sands China gained 5.315 per cent to trade at HK$26.75 with a turnover of 449.781 million, while Galaxy Entertainment traded up 3.704 per cent at HK$23.8 with a turnover of 337.451 million as of 2:20 pm.

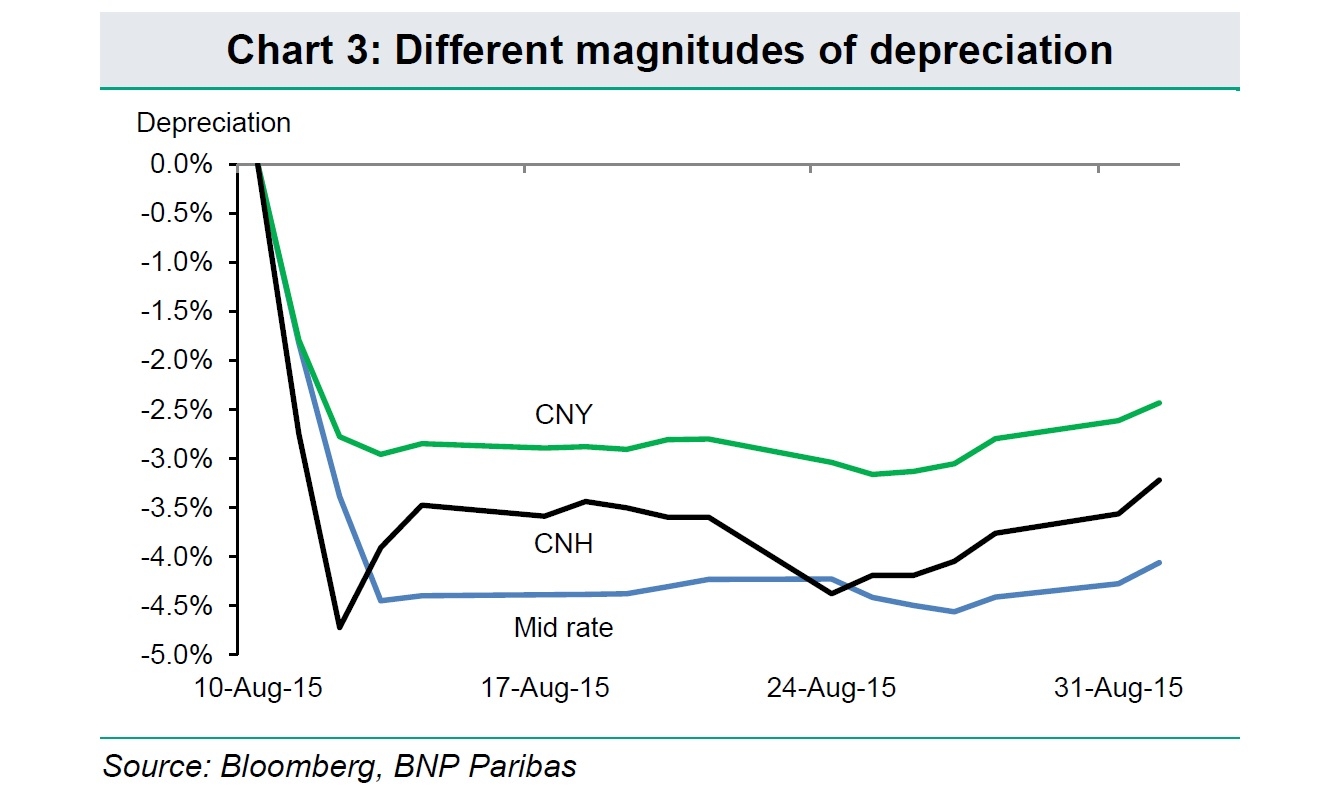

2:39pm: BNP Paribas chief china economist Chen Xingdong said:

“The People’s Bank of China (PBOC) had good reason to change its currency regime: to counter yuan overvaluation and meet IMF requirements for the yuan’s inclusion as an Special Drawing Rights (SDR) reserve currency.

The market believes, however, that the yuan is still overvalued and should have been allowed to depreciate far more (it is down a cumulative 4.2 per cent in the past 16 trading days). The central bank has been unwilling to let the currency depreciate too much, however, for political and economic reasons and has taken various measures to prop it up.

The PBOC has sold US dollar from its official FX reserves, required banks and firms to buy less and sell more hard currency, and demanded a deposit of 20 per cent on FX forward transactions. We expect the PBOC to keep the official USD/CNY fixing at 6.4 until November. What happens after that will depend on the IMF’s SDR decision, US Fed policy and China’s growth strategy.”

Clicks to enlarge all the charts from BNP.

{kind=link}

{kind=link}

{kind=link}

2:20pm: Hong Kong home prices will see an adjustment with an annual correction of 5-10 per cent in the next three years, according to JP Morgan.

The slowdown of Hong Kong's economy, plagued by falling retail sales and the softening mainland Chinese economy, will adversely affect home purchasing power and buying desire, said Cusson Leung, head of conglomerates and property research, J.P. Morgan.

“It is unlikely to see that home prices will see a sharp plunge of 30 per cent in a year. But the negative factors – such as declining retail sales and an anticipated rising unemployment rate – will be reflected since early next year. Home prices could see an adjustment of 5-10 per cent over the next three years starting 2016,” he said.

However, many home buyers have not felt the potential risk in the market and are still eager to enter it, said Leung.

2:11pm: The Hang Seng Index trades at 20,770.92, down 0.78 per cent or 164.02 points. The China Enterprises Index (H-share index), which track Hong Kong listed Chinese companies, trades at 9,103.68, down by 2.12 per cent or 197.64 points.

1:55pm: China’s oil giants Petro China and Sinopec hit their 52-week low during the afternoon session. Petro China lost 4.48 per cent to HK$ 5.76. Sinopec dropped 3.82 per cent to HK$ 4.79.

1:03pm The Hang Seng Index opens in the afternoon at 20,827.16, down 0.51 per cent or 107.78 points. The China Enterprises Index (H-share index), which track Hong Kong listed Chinese companies, opened the afternoon session at 9,090.08, down by 2.27 per cent or 211.24 points.

12:57pm: Chinese mutual funds saw the profits they made before the stock market peaked in June largely erased by the three-month long market rout.

The average returns for the stock funds over July and August stood at a negative 24.33 per cent, suggesting that 850 billion yuan of money was wiped out in the country’s mutual fund industry over the last two months, mainland newspaper China Economic Daily reports citing data from fund trackers.

12:07pm: The Hang Seng Index finished the morning 0.6 per cent lower at 20,809.5 while the H-share index fell steeply in the final hour of the session to close down 2.41 per cent at 9,077.54.

12:07pm: Greater China hedge funds saw their profits drop by an average 10 per cent for August, on track to post the biggest monthly fall since January 2000, according to data from Singapore-based hedge fund tracker Eurekahedge Pte.

11:35am: The Hang Seng Index is 0.5 per cent lower or by 104.05 points at 20,830.89. The H-share index is down 1.58 per cent, 147.35 points, at 9,153.97.

11:30am: Jefferies on fund flows between August 27 and September 2:

“Global equity markets experienced a return of net inflow of US$11 billion. The MSCI ACWI index rebounded a light 0.1 per cent for the week amid equity markets appearing oversold.

Despite emerging markets (EM) seeing a stronger rebound, up 1.2 per cent w-w, in equity performance terms, the region continued to witness net withdrawal. In other words, developed markets (DM) was the driver for the overall injection. Consequently, the trend that we have been experiencing year-to-date, i.e., switching to DM equities from EM equities, resumed.

In the global bond market, net withdrawal of US$1.2 billion remained intact while investors showed a clear preference among US/DM bonds over Europe/EM bonds geographically.

By category, government bonds for all duration remained the favorite with corporation and high yield bonds staying the opposite. For the first time in four weeks, investors were sellers, for a net US$651 million, among global commodity funds. The latest selling was broad-based by category. Lastly, investors unwind a net US$29 billion in the money markets. Europe and the US led the unwinding.

Among other asset classes, global bond funds witnessed their fourth straight weekly outflow. Meanwhile, the US$4.5 billion injection into the US bond market was a 22-week high. Majority of the buying went to government bonds, for all duration, and long-term corporate bonds.

Global commodities saw investors turning net sellers for US$651 million. The US$336 million withdrawal among Energy was the first outflow in 11 weeks. Global money markets witnessed a net withdrawal of US$29 billion. The European and the US money markets accounted for a withdrawal of US$12 billion each.”

{kind=link}

{kind=link}

{kind=link}

11:28am: Hong Kong dollar trades at 7.7505 against the dollar, near upper end of the currency peg. Euro/dlr stronger by 0.01 per cent at 1.1124. Dlr/yen at 119.57, weaker by 0.42 per cent. Pound/dlr weaker by 0.12 per cent to 1.5240. Australian dollar to US dollar weaker by 0.58 per cent to 0.6976.

10:57am: ABN Amro says the Euro is heading for parity against the US dollar by year end:

“The recent waves of risk aversion did not result in support for the euro. Instead the yen and the US dollar moved higher. This confirms our view that the spike higher in EUR/USD in August was not safe-haven demand related but merely the closing of euro short positions.

In addition, the increased likelihood for additional QE by the ECB has weighed on the euro this week. The ECB left monetary policy unchanged. It adjusted downwards its forecasts for growth and inflation, as expected.

There are two strong signals that the ECB will likely step up QE. For a start, the lower 2017 inflation forecast. Moreover, the ECB’s view that there are downside risks to the inflation outlook.

We remain bearish on EUR/USD mainly because of monetary policy divergence across the Atlantic. Our target for the end of 2015 for EUR/USD is parity.”

10:37am: The Hang Seng Index has dropped back from its earlier high and is now trading at 21,004.81, up 0.33 per cent or 69.87 points. The H-share index has also dropped during the morning session and is now down 0.54 per cent, 50.16 points, at 9,251.16.

10:07am: Early Movers in the Hong Kong market (biggest movers by turnover):

Chinese Internet firm Tencent was the highest traded stock Friday morning and is up HK$1.18 to HK$128.9. Insurer AIA is down 0.36 per cent at HK$41.35. China Construction Bank is up 0.38 per cent at HK$5.28. China Mobile is up 0.44 per cent at HK$92.15. Mainland insurer Ping An is up 0.54 per cent at HK$37.05.

9:55am: Ratings agency Fitch expects Macau’s economy to shrink 16 per cent in 2015:

“The contraction underscores the risks to Macao's economy from its heavy reliance on gaming revenues from Chinese visitors, and its vulnerability to shifts in mainland government policy. Gaming revenues have begun to stabilise in recent months, but the potential remains for substantial shifts to our forecasts - both on the upside and downside - with the evolving economic and policy conditions in China.

Fitch expects Macao's gaming revenues to drop by about 30 per cent in 2015, and the rapid pace of economic contraction thus far has been linked directly to the falling top line at casinos. The feed through to the broader domestic economy has been limited, though, as the impact has mostly been absorbed by casino operators through narrowing margins. All major casinos have nevertheless remained profitable, and unemployment has stayed low as hotels have sought to retain staff in advance of new casino resort openings in 2016-2017.

That said, there have been some signs that the domestic economy is beginning to slow. Household consumption and capital investment growth have fallen, albeit from a high base. Government has also announced measures to tighten spending, which will help to mitigate the impact on the fiscal account but may squeeze domestic demand. Risks are also growing to income growth and to Macao banks' loan growth, which could feed through to a further slowdown in the domestic property market.

Yet Fitch maintains a Stable Outlook on Macao's AA- rating, reflecting the territory's exceptionally strong sovereign balance sheet and external position. It has no debt liabilities, and retains fiscal reserves and accumulated surpluses in excess of 100 per cent of GDP - enough to almost cover six years of expenditures at the 2015 level projected by government. This gives the territory significant policy space to accommodate a structural shift in the economy and support diversification away from the current reliance on VIP gaming.”

9:52am: DBS Morning Call:

“The European Central Bank (ECB) left rates and scale of asset purchases unchanged on Thursday. Accompanying statements highlight emerging downside risks to growth, with inflation still below targets. Assurances that the present QE will run through September 2016 and can be extended beyond to meet the medium-term inflation goals, helped to send the euro sharply lower to 1.11-lows soon after.

The ECB stressed that the higher frequency indicators pointed to a “somewhat weaker economic recovery and a slower increase in inflation rates compared with earlier expectations”. Growth risks were seen from a slowdown in EM economies, which in turn depress global growth and crimp demand for euro area exports. Fallout of the ongoing turmoil in China is likely to be transmitted through trade channels hurting global exports and the confidence channel through financial markets.

The ECB cuts its forecasts for growth and inflation. Staff projections trimmed GDP estimates to 1.4 per cent in 2015, 1.7 per cent in 2016 and 1.8 per cent in 2017 (vs June’s assessment of 1.5 per cent, 1.9 per cent and 2 per cent respectively).

Inflation is expected to remain low and below-target at least over the next two/three years. Headline inflation is seen at 0.1 per cent in 2015, 1.1 per cent in 2016 and 1.7 per cent in 2017.

Base effects and gradual rise in oil in euro terms are expected to push up the energy component later this year. ECB chief Mario Draghi also added that the current QE program provided sufficient flexibility in terms of fine-tuning the size, consumption and duration of these purchases.

Since a low of 1.05/USD back in Mar, the euro has appreciated more than 7-8 per cent in recent weeks, in effect diluting the impact of the central bank’s asset purchases. With benchmark rates already at rock-bottom, we suspect that further policy support is likely to come by way of either an increase in the quantum or duration of the QE programme, should the need arise.”

9:50am: Offshore yuan trades at 6.4491 to the dollar, weaker from the previous close at 6.4480. Onshore yuan market was closed Friday for a holiday.

9:42am: From Agence France Presse:

The Nikkei-225 index at the Tokyo Stocks Exchange fell 0.63 percent or 114.65 points to 18,067.74 in mid-morning, after opening higher. The Topix index of all first section shares also dropped 0.69 percent or 10.22 points to 1,464.76.

9:37am: The Hang Seng Index is up 181.41 points, 0.87 per cent, at 21,116.35. The H-share index is 32.86 points stronger, 0.35 per cent, at 9,334.18.

9:10am: Hang Seng Index regular September futures are up 0.73 per cent or 151 points, at 20,850.

H-share index regular September futures are down 0.98 per cent or 90 points at 9,105.

9:09am: ING Morning Call:

“The revamped QE reinforces ECB’s determination to do all it can to support the Eurozone economy in the event recovery falters. President Mario Draghi’s dovish assessment was accompanied by downgrade of growth and inflation forecasts.

Bottom line: Weak global growth and rising policy accommodation by major central banks including China’s PBOC raise odds against Fed’s lift off this month for which tonight’s non-farm payroll data for August is key determinant (consensus 217k).”

8:51am: Rabobank Morning Call:

“Eurozone equities surging (Euro Stoxx +2.3 per cent) and EUR falling back to below 1.11 briefly: recall that we were above 1.17 on 24 August for a moment.

US stocks fared less well, opening strongly but then fading through the session (S&P +0.1 per cent), perhaps on the realization that there is a central bank round the corner looking like it is throwing out more favours than their own (and hence a profit-crimping stronger USD looms).

The fact that the US ISM services PMI beat expectations somewhat will also have encouraged that view.

Meanwhile, over in Japan things are looking less rosy due to the fact that so much QE has now been implemented that the Bank of Japan are running out of Japanese Government Bonds, and even T-bills, to buy.

That leaves the BOJ with three options: either stop increasing QE, in which case yen will start to appreciate again, dragging the country back into deflation; increase fiscal stimulus further, which would effectively be monetized by the BOJ, driving yen sharply lower again while making a nonsense of the pretence of ever emerging from this radical policy; or buy something else in vast quantities, such as ETFs, REITs, corporate bonds,...or perhaps even overseas assets?”

8:35am: Societe Generale says China’s FX reserves dropped US$150 billion last month:

“We estimate that China's FX reserves dropped by US$ 150 billion in August from US$3.65 trillion to US$3.50 trillion, compared with the US$50 billion decline in July. However, the possible range of declines in reserves could be anywhere from US$100 billion to US$200 billion.

The People’s Bank of China appeared to be heavily active in the spot market after the currency regime change on 11 August in order to stabilize the onshire yuan. Onshore yuan trading volume almost doubled in the 15 trading days following 11 August, compared to the previous 20 trading sessions and the YTD average.

The increase in onshore trading volume most likely reflected incremental dollar selling by local and foreign entities that was ultimately absorbed by the PBOC.

The last time trading volume spiked significantly was in March, and this was only a temporary increase lasting a few days. During that month, official FX reserves declined by US$71 billion, of which we estimate around US$40 billion was related to valuation effects.

Suspected intervention in the forward market via swaps might be a way for the PBOC to delay the impact of FX intervention on the current reading of official reserves, but such action, if there was, seemed to be taken only in the last few days of the month. In addition, the requirement of a foreign exchange risk reserve was announced on 1 September and should limit future swap activity.

Therefore, in our view, the most likely near term strategy of Chinese policymakers is to allow more oneshore depreciation to limit further appreciation in trade-weighted terms, in a largely controlled manner. And at the same time, (the implementation of) capital controls will probably be tightened on the margin, at least.”

Click on chart to enlarge.

{kind=link}

8:02am: Offshore yuan closed at 6.4480 on Thursday versus Wednesday finish at 6.4503.

7:57am: CICC analysts Wang Hanfeng and Li Qiusuo said:

“We believe the risks from stock pledges are unlikely to have a major impact on the financial system; the impact on the earnings of listed banks may be a mere 0.03 per cent, but the stock pledge business may be dampened while many investors are worried that the huge size of stock pledges (2.7 trillion yuan) may have a major impact on the financial system, we do not think so:

Firstly, the forced liquidation lines are generally set at 140 per cent/130 per cent. In other words, only if the prices of the pledged stocks decline by their daily limits for 3~4 consecutive days, would they come close to their forced liquidation lines, or if the pledgees are unable to sell off the positions, will they suffer book losses.

Secondly, we have conducted a scenario analysis on the impact of stock pledges on the financial system. Even if pledgees fail to sell the pledged shares or could not ask the pledgers to meet margin requirements, their current book losses from stock pledge agreements may just be 4.5 billion yuan.

The book losses of 2.6 billion yuan for brokerages account for 1 per cent of their operating revenue in 2014, while the 1 billion yuan at banks account for 0.03 per cent of the total net interest income of the banking sector in 2014.

Even assuming the share prices of pledged stocks plunge another 40 per cent (indicating the Shanghai Composite Index falls below 2,000 and the ChiNext to about 1,200), and the pledgees do not sell any pledged stocks, the book losses may be just 60.5 billion yuan, with the 34.5 billion at brokers accounting for 13 per cent of their operating revenue in 2014, and the 13.9 billion at banks accounting for 0.42 per cent of the total net interest income of the banking sector in 2014.

But the stock pledge business may be negatively impacted, which may force pledgees to introduce quantitative indicators, such as valuation and liquidity…We expect the pledgees to become more cautious after the recent market corrections, and the pledge ratio will be set based on more standards such as valuation and liquidity.”

Click on the charts below to enlarge.

{kind=link}

{kind=link}