Is HSBC’s Canada sale to RBC enough to placate critics like Ping An as it doubles down on Asia?

- Lack of scale, international connectivity a driving factor as HSBC agreed this week to sell Canadian operation to Royal Bank of Canada for US$10 billion

- Slightly smaller than mainland China in terms of deposits held, Canada business has been profitable for the past decade, outpacing its US operations

On the surface, the Canadian business would seem to have been the perfect fit for HSBC’s strategy of serving wealthy customers and businesses from China and other parts of Asia internationally.

Its biggest concentration of branches are in urban areas favoured by new immigrants from Asia, such as Toronto and Vancouver, and more than 1.8 million people, or about 5 per cent of Canada’s population, identify themselves as being of Chinese descent.

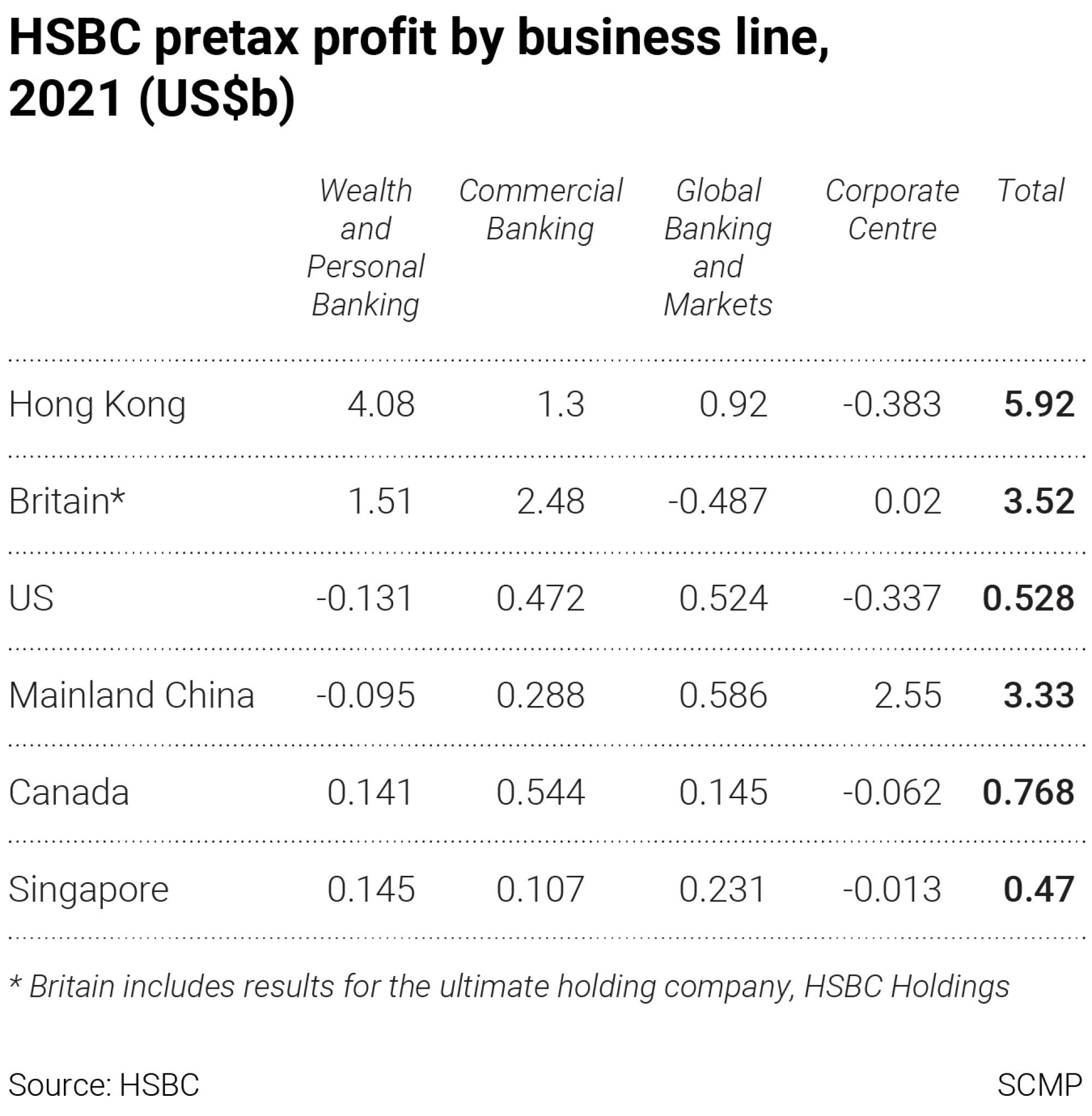

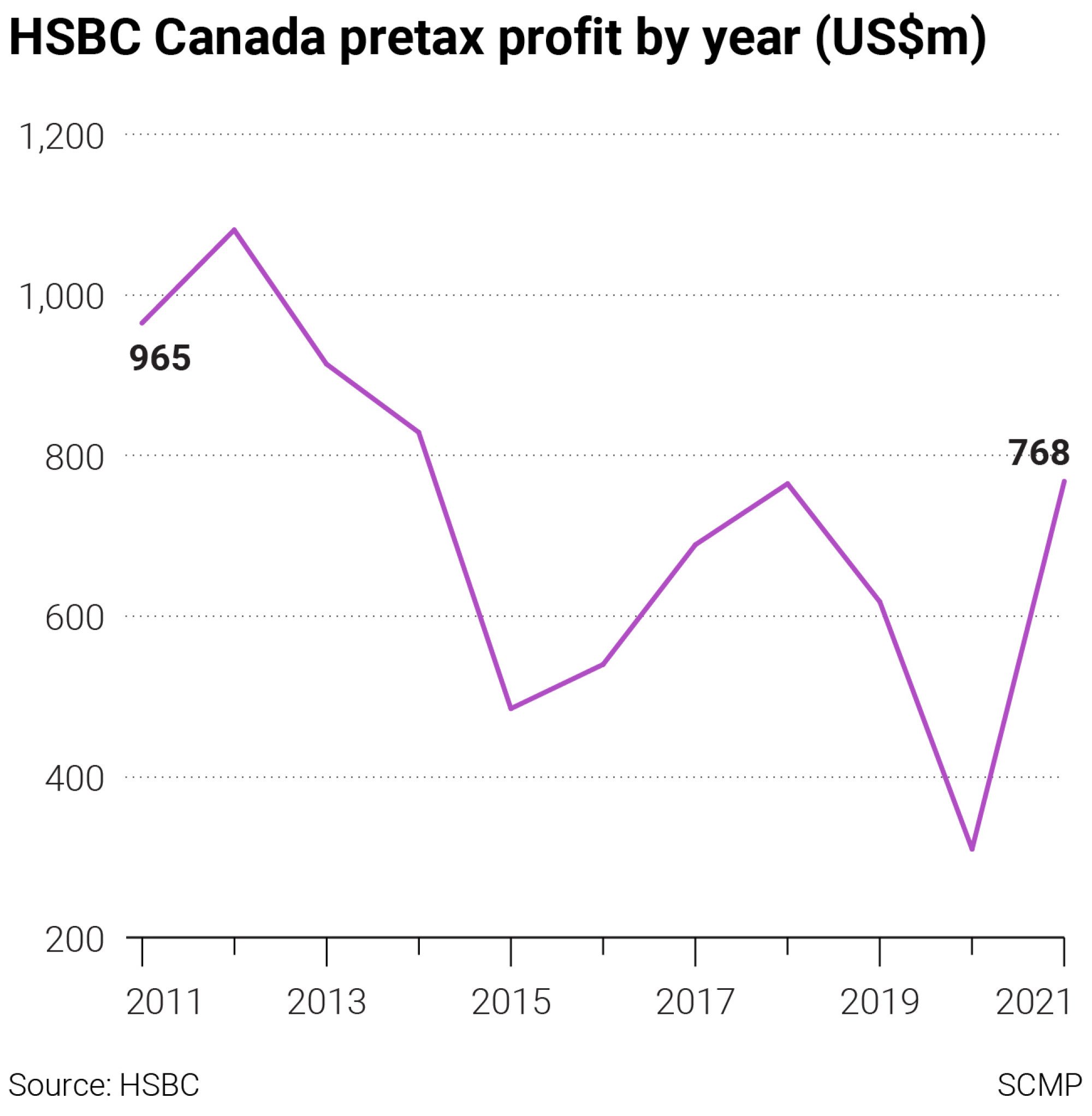

Plus, it has been consistently profitable, outpacing the bank’s much larger United States operations on a pre-tax basis over the past three years despite holding about half the amount of customer deposits. Last year alone, the Canadian business generated a pre-tax profit of US$768 million versus US$528 million in the US.

05:25

HSBC’s break-up dilemma: why bank’s largest shareholder is pushing for change

“Although HSBC is a global bank, most of its revenue has come from the Asia-Pacific market in recent years, and the business in the Asia-Pacific region has also shown a relatively strong growth trend,” said Kenny Ng Lai-yin, a strategist at Everbright Securities International. “Therefore, selling the Canada business is believed to be a strategic consideration, by which HSBC can concentrate more resources on the Asia-Pacific market.”

The sale of HSBC’s Canadian business comes in the wake of immense pressure from its biggest shareholder Ping An, to spin-off the Asian business. HSBC, based in London, generates much of its profit in Asia.

“We suggest HSBC should also plan ahead and think of what a ‘new global model’ should look like, carefully evaluating the value and business contribution of each aspect, while striking a balance between its global finance model and cross-border systemic and geopolitical risks to achieve long-term, sustained and steady operation,” he said. “Just divesting a few small markets or businesses will not fundamentally solve these issues.”

His remarks were some of the most pointed public comments since the Chinese insurer, which last held an 8.3 per cent stake in HSBC, began its unorthodox media campaign to break up the bank, ahead of its annual shareholders’ meeting in April.

HSBC CEO Noel Quinn and other executives have countered that the bank generates much of its business through its international network, and separating the Asian business would require creating an entirely different information technology network for the spun off business at great expense. The bank operates in 63 countries and territories worldwide.

HSBC executives said the Canadian business has performed well, particularly following the coronavirus pandemic, but lacks the scale to compete with bigger players in Canada, particularly when compared with HSBC’s footprint in other markets.

“Our market share in Canada is about 3 per cent,” Quinn said on the bank’s recent third-quarter results call. “It’s largely a domestic business. Our Canadian business, particularly in wholesale banking and supply chain finance, is less internationally connected than many other markets that we operate in.”

HSBC Canada’s loan portfolio is split “fairly evenly” between residential mortgages on one side and commercial and corporate loans on the other, according to RBC. It has about 800,000 clients in Canada.

HSBC, which traces its roots back 157 years to Hong Kong and Shanghai, at one point marketed itself as the “world’s local bank”, with outlets in 81 markets around the world.

However, its global ambitions have shrunk somewhat in recent years as the bank has pulled back from markets and shifted capital from underperforming businesses in the West to growth markets in Asia.

Exports from Canada to China have also declined 14.4 per cent to C$12.4 billion in the first half of the year, according to the University of Alberta’s China Institute.

It also is the latest in a series of divestitures since Quinn became CEO in 2019. The lender is selling its French retail banking business to a unit of private equity giant Cerberus and agreed in July to offload its Russian operations to Expobank.

“Asia may have high growth now but the situation may not last forever,” said Sandra Mak, a Hong Kong shareholder who has bought shares at various times since 1981 and welcomed the sale of the Canadian business. “HSBC should still maintain a strategy to have international exposure for it to capture growth in different markets to diversify the risk.”

HSBC entered Canada in 1981 and had 12 branches four years later.

It made about a dozen acquisitions, including Bank of British Columbia in 1986, to expand its business over time, becoming the seventh largest bank in Canada. It now has about 130 branches and 4,200 employees across Canada and C$134 billion in assets.

In the first nine months of this year, the Canadian business reported a pre-tax profit of C$788 million on revenue of C$1.83 billion, according to HSBC. That compared with a pre-tax profit of C$725 million on revenue of C$1.64 billion for the prior-year period.

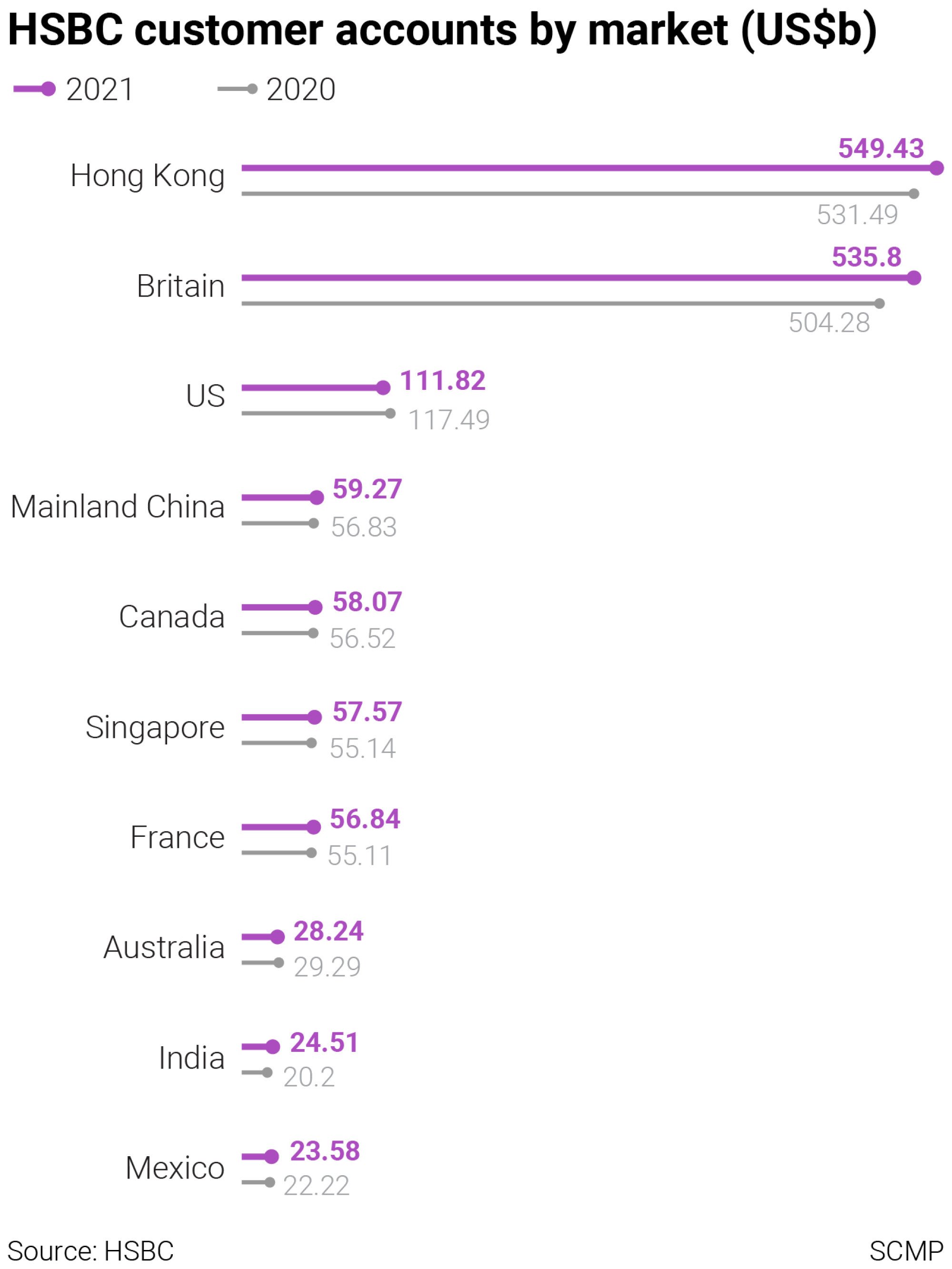

In terms of customer accounts, the Canadian business held US$58.1 billion in deposits at the end of 2021, making it the bank’s fifth biggest market. By comparison, HSBC’s Hong Kong business, its largest market, had US$549.4 billion in customer accounts at the end of last year, while the mainland China business had US$59.3 billion and Singapore had US$57.6 billion.

The Canadian business reported a return on average shareholders’ equity ratio of 14.7 per cent in the first three quarters of the year. That is better than the overall bank’s return on tangible equity ratio (ROTE) of 10.8 per cent through the nine months ended in September and ahead of its target of a ROTE exceeding 12 per cent next year.

“HSBC Canada has been an important and profitable contributor to the group’s operating performance, though small relative to certain other HSBC subsidiaries,” said Daniel Da Silva, a credit analyst at S&P Global Ratings, in a research report. “Its well-established retail and commercial banking franchise in western Canada, its expanding presence in Ontario, and the support of the parent have afforded it our core status designation to the parent.”

For Royal Bank of Canada, the transaction will position the lender as the “bank of choice” for commercial clients with international needs and give it greater access to affluent clients seeking wealth management products and newcomers to Canada as immigration is expected to increase materially in the coming years, according to Dave McKay, RBC’s president and CEO.

“It will also help us better serve global clients looking to invest and grow in Canada, which is key for the country’s economic growth and prosperity,” McKay said.

RBC is one of Canada’s biggest banks, with C$1.71 trillion in assets at the end of last year and more than 92,000 employees.

The deal is expected to enhance RBC’s product offerings, in part because of HSBC’s trade finance and multicurrency product offerings, McKay said. It also will better position RBC with affluent customers, particularly international clients with connections to Canada.

“It’s a unique, once-in-a-generation opportunity to leverage all of the investments we’ve already made to enhance a world-class retail and commercial bank,” McKay said.

HSBC said its board was “proactively” considering a one-off dividend or share buy-backs to return “an appropriate amount of additional surplus capital” from the transaction. The deal is expected to result in an estimated pre-tax gain of US$5.7 billion.

Returning capital, particularly through a dividend, would be important to a shareholder base that saw HSBC’s dividend suspended in 2020, as HSBC’s chief regulator in Britain asked lenders to hold onto capital to ensure banks could support the economy during the Covid-19 pandemic.

The bank’s shareholders in Hong Kong are particularly reliant on dividend payouts, which have trailed pre-pandemic levels since they resumed last year.

“Many minority shareholders of HSBC are happy to learn about the sale of the Canadian business of the bank,” said Sai Kung district councillor Christine Fong Kwok-shan, who is not an HSBC shareholder, but represents 500 shareholders with a combined stake of less than 5 per cent who challenged the bank’s management over the dividend suspension.

“They are happy about the sale as they welcome the idea that HSBC may consider delivering a special dividend or interest from the proceeds of the sale,” she said.

Despite its strong performance, the footprint of HSBC’s Canadian business was increasingly out of step with the bank’s international strategy.

“Three quarters of revenues are generated in wealth and personal banking, reflecting a lower proportional connection to HSBC’s leading global trade network than in other countries,” BofA Securities analyst Alastair Ryan said in a research note.

During HSBC’s third-quarter call, Quinn contrasted the difference between Canada and HSBC’s business in Mexico, which he said he had no intention of selling.

Depending on the product line, HSBC has a 7 per cent to 10 per cent market share in Mexico and “significant upside potential”, particularly as an international bank operating in the country, Quinn said.

“We believe that the supply chain interconnectivity between Mexico, the rest of the world and the US will actually increase in volume of business and business opportunity because it is an important manufacturing base into the US, and that is at the core of what we do.

“And, we have a very strong market share position in retail banking in Mexico with strong interconnectivity between retail and corporate banking in Mexico as a result of the payroll services.”